An FHA loan can be a helpful path to homeownership, especially if you’re buying your first home, have limited savings or are working on your credit.

Backed by the Federal Housing Administration, FHA loans are designed to make homebuying more accessible. They often come with lower down payment options and more flexible credit requirements than many conventional loans. Still, every loan option has trade-offs.

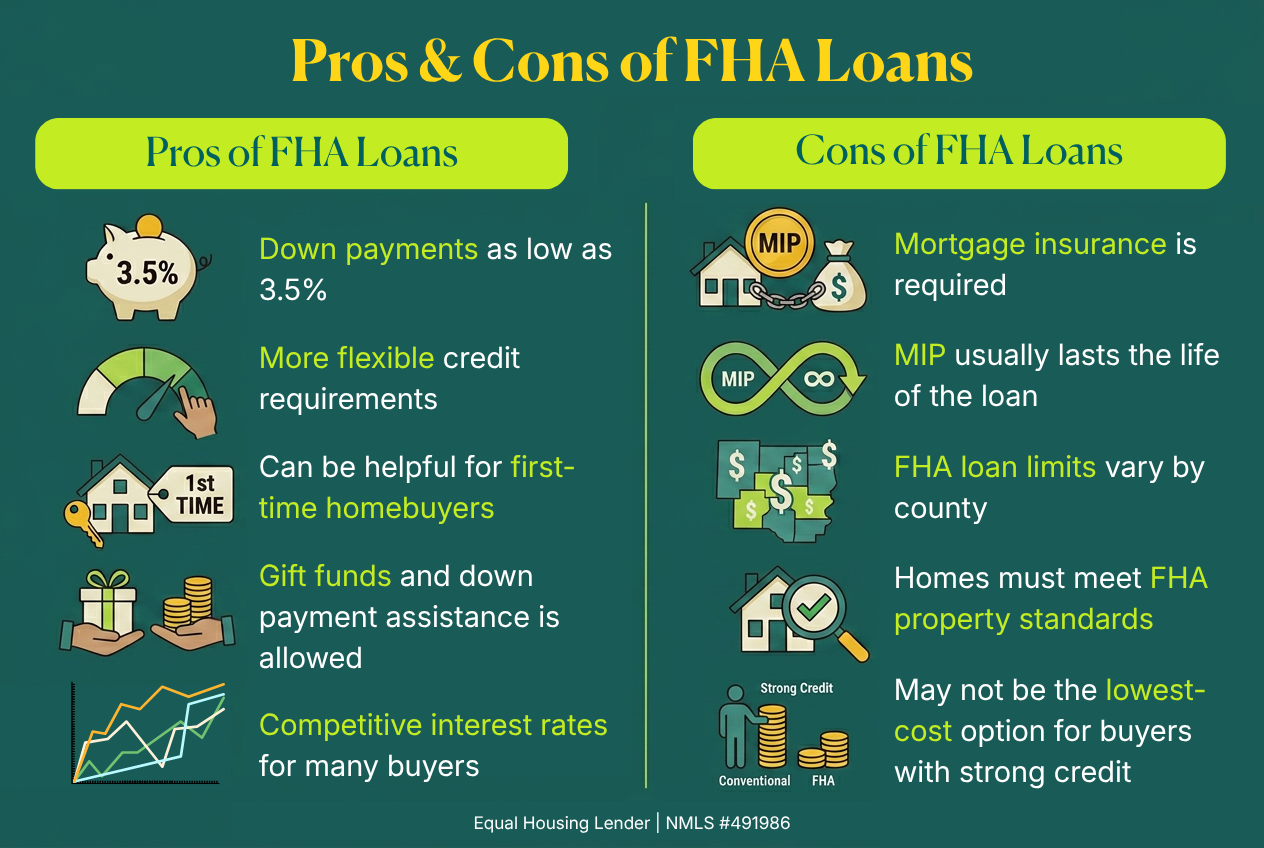

Here’s a clear look at the pros and cons of FHA loans so you can decide whether this option fits your homebuying goals.

In a Nutshell

FHA loans can make it easier to buy a home, but they may cost more over time than some conventional loans. Here’s a quick look at the biggest pros and cons of FHA loans.

What Is an FHA loan?

An FHA loan is a mortgage insured by the Federal Housing Administration and offered through FHA-approved lenders.

Because the FHA insures the loan, lenders may be able to offer more flexible requirements than they would with some conventional loans. That flexibility can help buyers who have lower credit scores, smaller down payments or a shorter credit history.

FHA loans are especially common among first-time homebuyers, but you do not have to be a first-time buyer to use one.

Benefits of FHA Loans

1. Low Down Payment Requirement

One of the biggest benefits of an FHA loan is the low down payment requirement.

If your credit score is 580 or higher, you may be able to qualify with as little as 3.5% down. On a $300,000 home, that would be a $10,500 down payment.

If your credit score is between 500 and 579, FHA guidelines require a larger down payment of at least 10%. HUD also notes that borrowers with a credit score below 500 are not eligible for FHA-insured financing.

Note: Individual lenders can enforce their own credit guidelines above the minimums. Neighbors Bank typically requires 620+.

2. More Flexible Credit Requirements

FHA loans are known for being more flexible with credit than other types of loans. For conventional, you typically need a 660+ to qualify for a 3% down payment, while FHA guidelines allow scores as low as 580 for 3.5% down, or 500 to 579 with 10% down. However, it’s important to know that individual lenders may set their own requirements above the FHA’s minimums.

That means an FHA loan may be worth exploring if your credit has a few bumps, but you’re ready to take steps toward homeownership.

3. Competitive Interest Rates

FHA loans have competitive interest rates, especially for buyers whose credit scores make conventional loan pricing more expensive.

Your exact rate will still depend on your full financial picture, including your credit score, down payment, loan amount and current market conditions. The important thing to remember is that the interest rate is only one part of the total cost. FHA mortgage insurance can affect your monthly payment and long-term cost, too.

4. Gift Funds and Down Payment Assistance are Allowed

FHA loans allow for the use of gift funds or approved down payment assistance to help cover your down payment or closing costs.

That can be a big help if you have a steady income but need support with the upfront cash needed to buy a home.

5. FHA Loans Can Help Buyers Start Building Equity Sooner

For some buyers, the biggest advantage of an FHA loan is timing.

If saving 10% or 20% down would take several more years, an FHA loan could help you buy sooner with a smaller down payment. That gives you a chance to start building equity and creating stability in a home of your own.

This does not mean rushing into a home before you’re ready. It means FHA loans can be one way to make homeownership feel more achievable when the main obstacle is upfront savings.

Disadvantages of FHA Loans

1. FHA Mortgage Insurance Is Required

FHA loans require mortgage insurance premiums called MIP for short. There is an upfront premium and an annual premium.

The upfront MIP is a one-time cost (1.75% of your loan amount) that most people roll into their loan costs, while the annual MIP is broken into monthly payments and included with your mortgage payment.

The annual MIP amount depends on factors like your loan amount, loan term and down payment. Because it adds to your monthly payment, it’s important to include FHA mortgage insurance when comparing the true cost of an FHA loan against other mortgage options.

2. MIP May Last for the Life of the Loan

This is one of the biggest FHA loan drawbacks.

If you put less than 10% down on an FHA loan, FHA mortgage insurance lasts for the life of the loan. If you put 10% or more down, MIP can be removed after 11 years.

That’s different from conventional loan private mortgage insurance, or PMI, which can be removed once you reach 80% home equity, while FHA MIP generally does not fall off based on equity alone.

Some buyers choose to refinance from an FHA loan into a conventional loan later, once their credit, equity or finances improve. Refinancing is not guaranteed and depends on your situation at the time, but it can be part of a longer-term plan.

3. FHA Loan Limits May Affect How Much You Can Borrow

FHA loans have county-based loan limits. That means the maximum amount you can borrow with an FHA loan depends on where the home is located.

For 2026, HUD lists the FHA one-unit loan limit floor at $541,287 and the high-cost area ceiling at $1,249,125.

If you’re buying in a higher-cost area, an FHA loan may not cover the price range you’re looking at. In that case, a conventional loan or another mortgage option may be a better fit.

4. FHA Appraisals Include Property Standards

Like other mortgage appraisals, an FHA appraisal helps confirm the home’s value. But FHA appraisals also look at whether the home meets FHA’s minimum property standards.

The goal is to make sure the home is safe, secure and livable. The appraiser may flag issues such as peeling paint, exposed wiring, safety concerns, structural problems or other repairs that need to be completed before closing.

This can protect you from buying a home with serious issues, but it can also add time or cost if repairs are needed.

5. FHA Loans May Not Be the Cheapest Option for Every Buyer

FHA loans can be a strong fit for buyers with limited savings or lower credit scores. But if you have strong credit, a larger down payment or enough income to qualify comfortably, a conventional loan usually costs less over time.

That’s why it helps to compare the full picture, not just the down payment. Look at the interest rate, mortgage insurance, closing costs, monthly payment and how long you plan to keep the loan.

FHA vs. Conventional Loan Pros and Cons

Here’s a simple side-by-side look at how FHA and conventional loans compare.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Down payment | As low as 3.5% with a 580+ credit score | Some options may allow as low as 3% for qualified buyers |

| Credit score | FHA allows lower credit scores, though lenders may set higher minimums | Often 620 or higher |

| Mortgage insurance | MIP for the life of the loan, unless 10% down payment at closing | PMI usually required with less than 20% down, removable at 20% equity |

| Mortgage insurance removal | Often lasts for the life of the loan with less than 10% down | PMI may be removable once enough equity is reached |

| Property standards | FHA appraisal includes minimum property standards | Appraisal requirements are generally less strict |

| Loan limits | County-based FHA limits | Conventional loan limits may be higher in many areas |

| Best fit | Buyers with limited savings or lower credit | Buyers with stronger credit or more savings |

As you can see above, FHA loans are ideal for buyers who may not qualify for conventional loans due to lower credit scores or limited down payments. However, conventional loans provide greater flexibility and can be less costly over time, particularly for borrowers who meet the credit and down payment requirements.

Is an FHA Loan a Good Choice For You?

FHA loans open doors for those who meet certain criteria, offering a more accessible homebuying path. Here are a few situations where an FHA loan may be a good fit:

First-Time Homebuyers with Limited Savings: If you're diving into the housing market for the first time and don't have a hefty down payment, an FHA loan can make your dream home a reality with just 3.5% down.

Buyers with Less-Than-Perfect Credit: If your credit score isn't up to par for conventional loans, FHA loans offer a lifeline. With more lenient credit requirements, you can secure financing with manageable interest rates and payments, even if your credit history has a few bumps.

Those Planning to Refinance in the Future: If you’re buying now with the intention of improving your finances down the road, an FHA loan could be a wise starting point. You can get into your home now and potentially refinance later into a conventional loan, saving you money by eliminating the lifetime mortgage insurance premium.

If you’re unsure which loan option is best for you, reach out to a Neighbors Bank loan specialist today. We're here to help guide you through the process.

With over 11 years in the mortgage industry, Matt Roy has spent the last 7 years as an underwriter. He’s passionate about understanding the “why” behind lending decisions and helping homebuyers succeed.