Many renters in the U.S. have put homeownership on the back burner. Most haven't given up, but the path feels out of reach right now.

Neighbors Bank surveyed 1,011 moderate-income renters to understand what's driving that feeling and how their homebuying assumptions compare to what is actually required. We also asked what would help them move forward. Here's what we found.

Key Takeaways

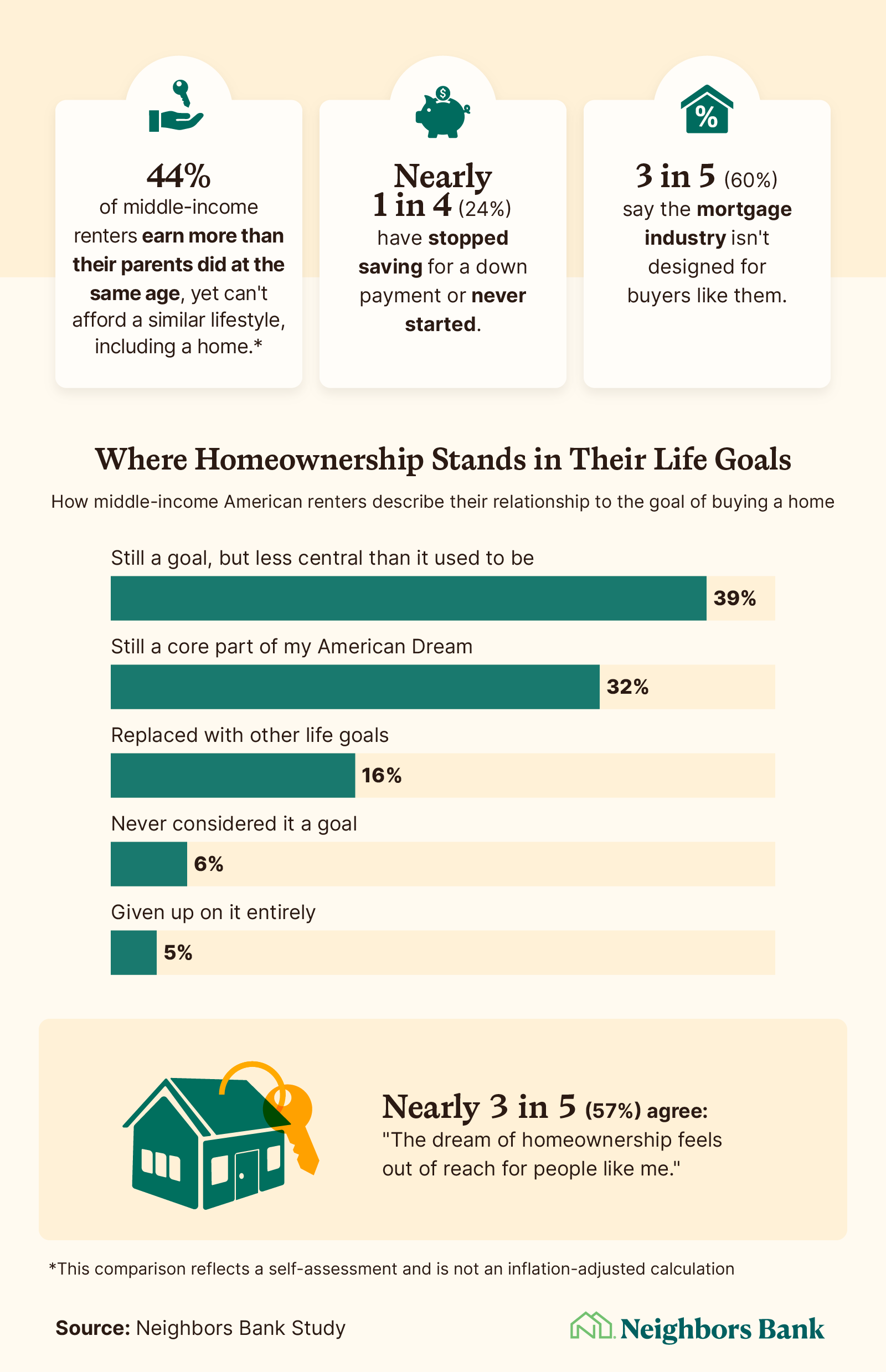

Nearly 1 in 2 middle-income renters (44%) earn more than their parents did at the same age, but still can't afford a home.*

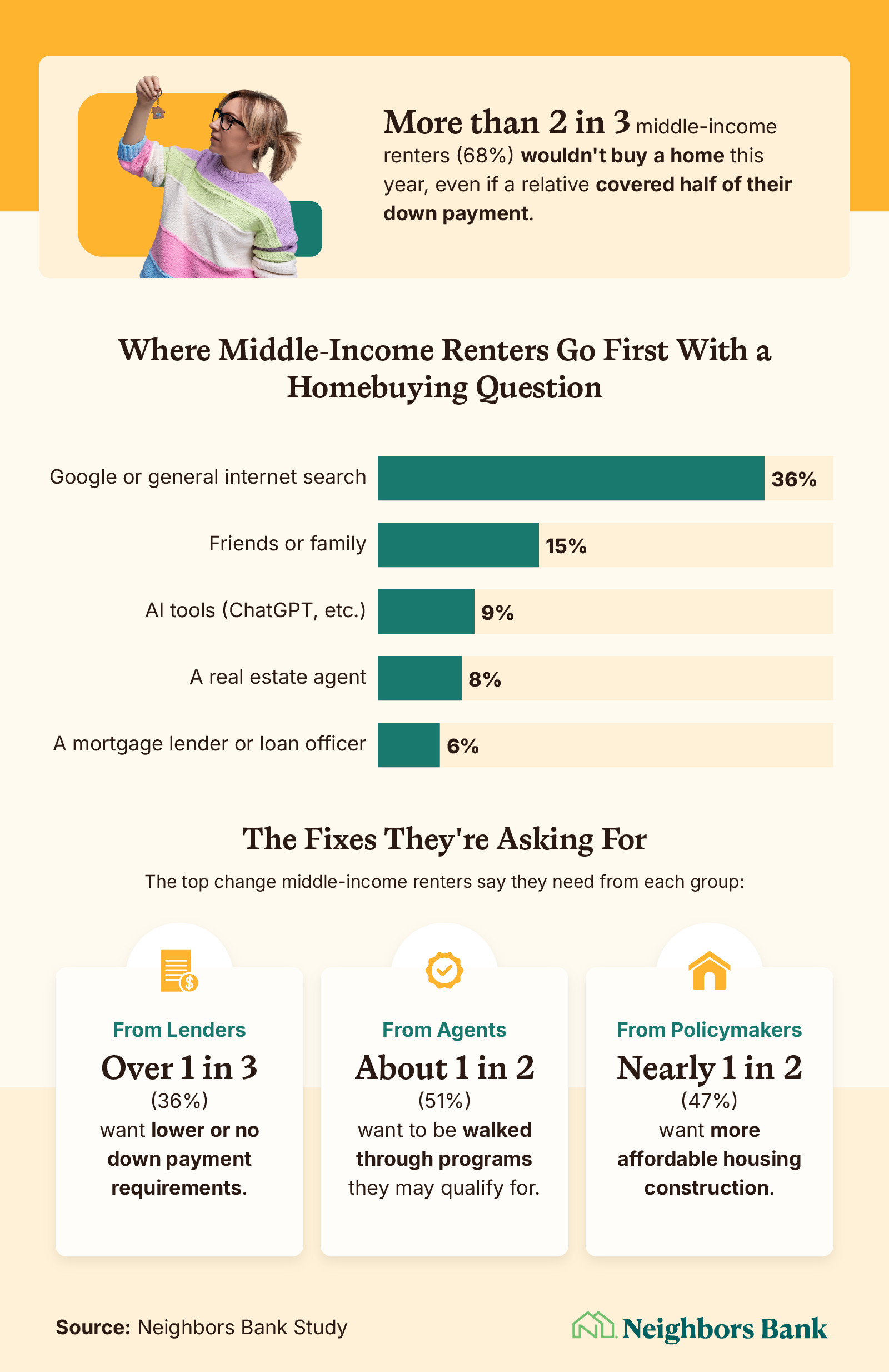

More than 2 in 3 middle-income renters (68%) wouldn't buy a home this year, even if a relative covered half their down payment.

Nearly 3 in 5 middle-income renters (57%) say the dream of homeownership feels out of reach for people like them.

3 in 5 middle-income renters (60%) say the mortgage industry isn't designed for buyers at their income level.

Nearly 1 in 4 middle-income renters (24%) have stopped saving for a home or never started.

*Respondents’ comparisons to their parents’ earnings reflect the respondents’ own assessments rather than an inflation-adjusted calculation.

The Dream of Homeownership Deferred

For a significant number of American renters, the goal of buying a home has slipped out of focus.

Nearly 1 in 2 middle-income renters (44%) said they currently make more than their parents did at the same age but can't afford a similar lifestyle, including a home. About 1 in 3 (32%) still consider owning a home a core part of their American Dream, while 39% said it remains a goal but is less important than it used to be. The rest had moved on, partially or fully: 16% replaced homeownership with other life goals, 6% never considered it a goal, and 5% had given up on it entirely.

More than half of middle-income renters (60%) said the mortgage industry isn't designed for buyers at their income level. Nearly 3 in 5 (57%) said the dream of homeownership feels out of reach for people like them. Almost 1 in 4 (24%) had stopped saving for a down payment or never started.

The pressure didn't land evenly. American women were more likely than American men to have stepped back from the goal:

Nearly 1 in 3 middle-income women (28%) had stopped saving for a home or never started, compared with 16% of men.

More middle-income women (61%) than men (49%) said the dream of homeownership feels out of reach for people like them.

Generations also told different stories. Gen Z renters reported the most optimism overall, but were stretching toward the most competing goals at once:

More than 4 in 5 Gen Z renters (83%) said they're likely to own a home in their lifetime, the highest of any generation.

Nearly 1 in 4 (25%) had never started saving for a down payment, the highest of any generation.

Gen Z was most likely to say that owning a home is necessary for a sense of belonging in their community (67%).

2 in 3 (67%) also said they'd feel they missed a major life milestone if they never owned a home, compared with 51% of Gen X.

Gen Z renters are saving for travel (48%), a major purchase (33%), starting a family (27%), and further education (25%) at the same time as a home.

As for Gen X, they were less likely to imagine a buying window and more skeptical of the system:

1 in 5 Gen X renters (21%) said they don't believe they'll ever own a home, the highest of any generation.

Nearly 2 in 3 Gen X renters (64%) said the mortgage industry isn't designed for buyers at their income level.

The Math Renters Think They Need to Own a Home

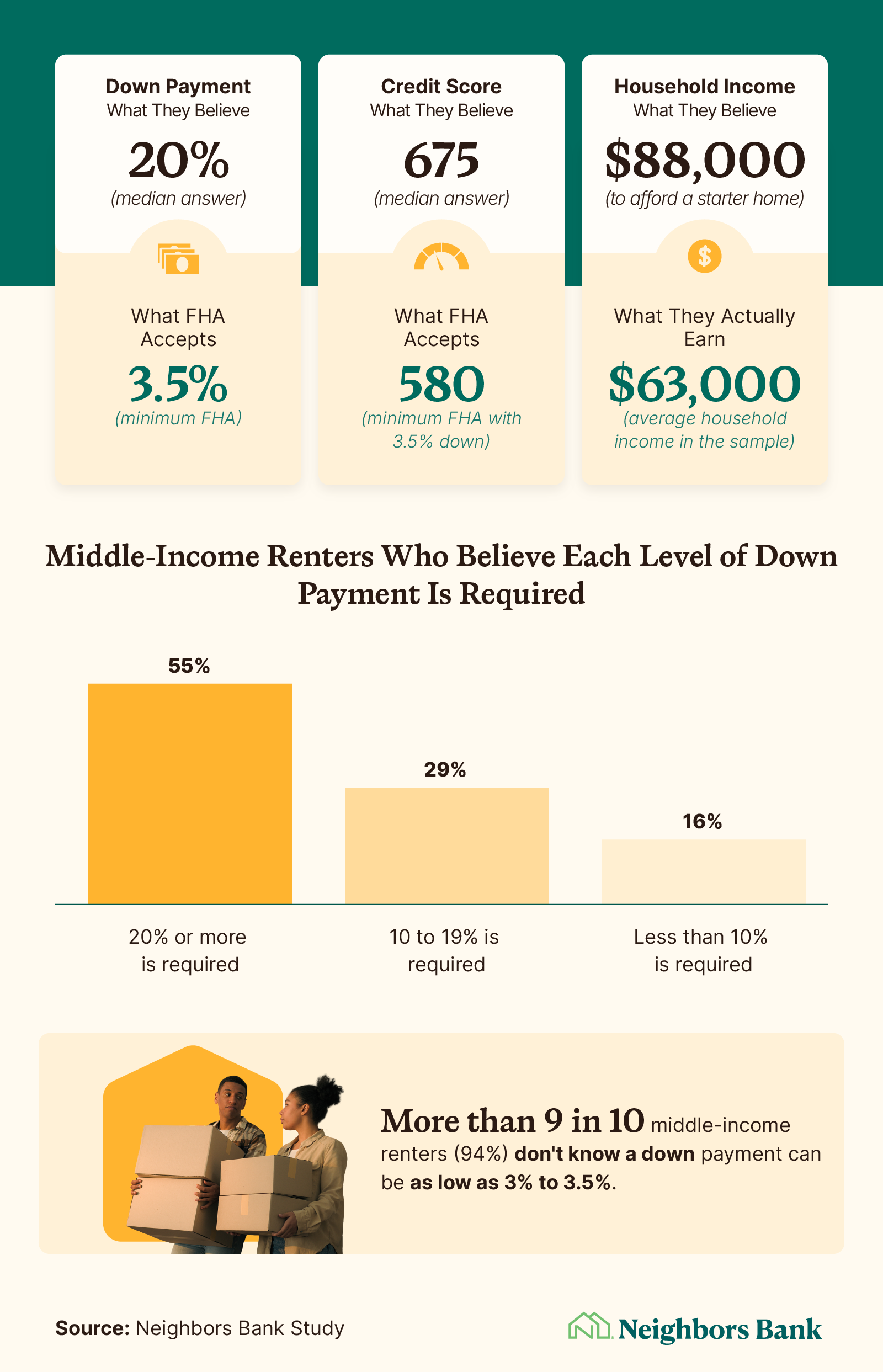

The numbers middle-income renters carry around in their heads have less to do with what's required to qualify for Federal Housing Administration (FHA) loans and more to do with rules of thumb that have hardened over a generation.

When asked what they believed a starter home requires, the median respondent said a 20% down payment, a 675 credit score, and an $88,000 household income. Respondents estimated the required income was roughly 40% higher than their current earnings. However, for an FHA loan, lenders are more interested in a steady employment and income history over the past two years than a set income level.

More than half of middle-income renters (55%) believe a 20% or larger down payment is required, while 29% think 10% to 19% is required, bringing the share who overestimated the minimum to more than 4 in 5 (84%). Just 16% believed less than 10% is required. More than 9 in 10 (94%) didn't know a down payment could be as low as 3% to 3.5%.

Credit score expectations followed the same shape. Just 8% guessed at or below FHA's actual 580 minimum, while nearly 1 in 2 respondents (45%) believed a score of 700 or higher is required to qualify. More than 1 in 4 (28%) said putting less than 20% down is financially irresponsible, even when loan programs allow it.

What most middle-income renters don't see are the loan programs already built for buyers in their position. FHA loans require as low as a 3.5% down payment for borrowers with a 580 credit score, though keep in mind that individual lenders often require a higher score to qualify. USDA loans allow for a $0 down payment for buyers in eligible rural and suburban areas, and VA loans offer a $0 down payment for qualifying service members, veterans, and surviving spouses. Conventional 97 loans bring the minimum down payment to 3% for eligible first-time buyers. Each program has its own qualification path, but the floor is far lower than the 20% rule of thumb most respondents named.

The perception gap can delay timelines or stretch them indefinitely. A third of middle-income renters (33%) said they're at least six years away from buying a home, or believe they never will be. Nearly 2 in 5 Gen Z renters (39%) said the same, the highest of any generation. More than 1 in 4 respondents (27%) said they felt further from buying today than they did three years ago, climbing to 1 in 3 (33%) among renters earning $50,000 to $74,000 and 34% among Gen X.

What Would Get Renters Off the Sidelines

If the math is the wall, the obvious question is what would help renters get over it. For most respondents, the answer wasn't quick.

More than 2 in 3 middle-income renters (68%) said they wouldn't buy a home this year even if a relative covered half their down payment. About 1 in 3 (32%) said they would. The rest pointed to other obstacles:

25% said they still need to save more on their own end.

14% said home prices in their area are still too high.

13% said their income or job stability isn't there yet.

More than 1 in 10 Gen Z renters (11%) said lifestyle reasons, such as not being ready to settle down or planning to move, are their biggest barrier, nearly double the overall rate of 7%.

Where renters go first for a homebuying question says almost everything about where they're getting their information. Google or a general internet search was the first stop for 36% of respondents. Friends or family came next at 15%, followed by AI tools (9%). Fewer relied on real estate agents (8%), mortgage lenders or loan officers (6%), and government websites (3%).

Just 2% of Gen Z middle-income renters went to a mortgage lender first when they had a homebuying question, the lowest of any generation. They were 10 times more likely to ask friends or family first (21%). Nearly 1 in 2 middle-income renters (46%) had never researched a single homebuying assistance program in depth, despite 90% being aware of at least one.

When asked what would help move them toward homeownership, respondents pointed to three different groups for three different fixes:

From lenders: More than 1 in 3 (36%) wanted lower or no down payment requirements. The share climbed to more than 2 in 5 Gen X renters (43%), compared with 3 in 10 Gen Z renters (30%).

From real estate agents: About 1 in 2 (51%) wanted to be walked through programs they may qualify for.

From policymakers: Nearly 1 in 2 (47%) wanted more affordable homes built in their area.

Closing the Reality Gap

The perception and information gaps this survey turned up are likely keeping many middle-income renters out of the housing market. Buyers who feel locked out today could qualify for loans if they knew more about loan options, requirements, and assistance programs. Closing these gaps won't fix every barrier, but it could help many achieve their dream of homeownership. If you're not sure where you stand, let's find out together today.

Methodology

Neighbors Bank surveyed 1,011 moderate-income American renters to understand how they perceive the path to homeownership. For this study, middle-income was defined as a household income of $40,000 to $125,000, capturing renters between roughly 60% and 120% of national area median income. Respondents were asked what they believe a down payment, credit score, and household income required to buy a home look like, how their saving and homeownership goals have shifted over time, where they go first for homebuying information, and what changes from lenders, real estate agents, and policymakers would most increase their confidence to apply. Respondents’ comparisons to their parents’ earnings reflect the respondents’ own assessments rather than an inflation-adjusted calculation. Generationally, 23% were Gen Z, 58% were millennials, 16% were Gen X, and 3% were baby boomers.

About Neighbors Bank

Neighbors Bank believes homeownership should be affordable, accessible, and achievable for everyone. We're licensed in all 50 states and offer home loan options that can cover up to 100% of the down payment and closing costs, so savings don't have to be the thing that stops you. Whether you're just starting to explore your options or ready to take the next step, we'll walk you through it.

Fair Use Statement

This content may be shared for noncommercial purposes only with proper attribution to Neighbors Bank. When referencing or reposting these findings, please include a link back to Neighbors Bank.