Saving for a home down payment can look different depending on where you live and what you do for work. As a lender dedicated to helping everyday Americans become homeowners, Neighbors Bank wanted to understand how affordability breaks down across the country for both typical families and the everyday workers who keep communities running.

We analyzed how long it would take workers in seven occupations to save for a 3% starter-home down payment across the 50 largest U.S. metro areas, and asked the same question for a typical family, defined by the Census Bureau as two or more related people living together, earning the local median income. We found that homeownership is still within reach for many workers and families across the country, and knowing your local market is one of the best first steps you can take.

This study measures the time it takes to save a 3% down payment, not the traditional 20%. A 3% down payment is one of the lowest conventional options available to many first-time buyers through loan programs backed by Fannie Mae and Freddie Mac, subject to credit approval and program eligibility requirements. We used 3% to show that homeownership can be far more attainable than the 20% benchmark many people assume they need.

In a nutshell

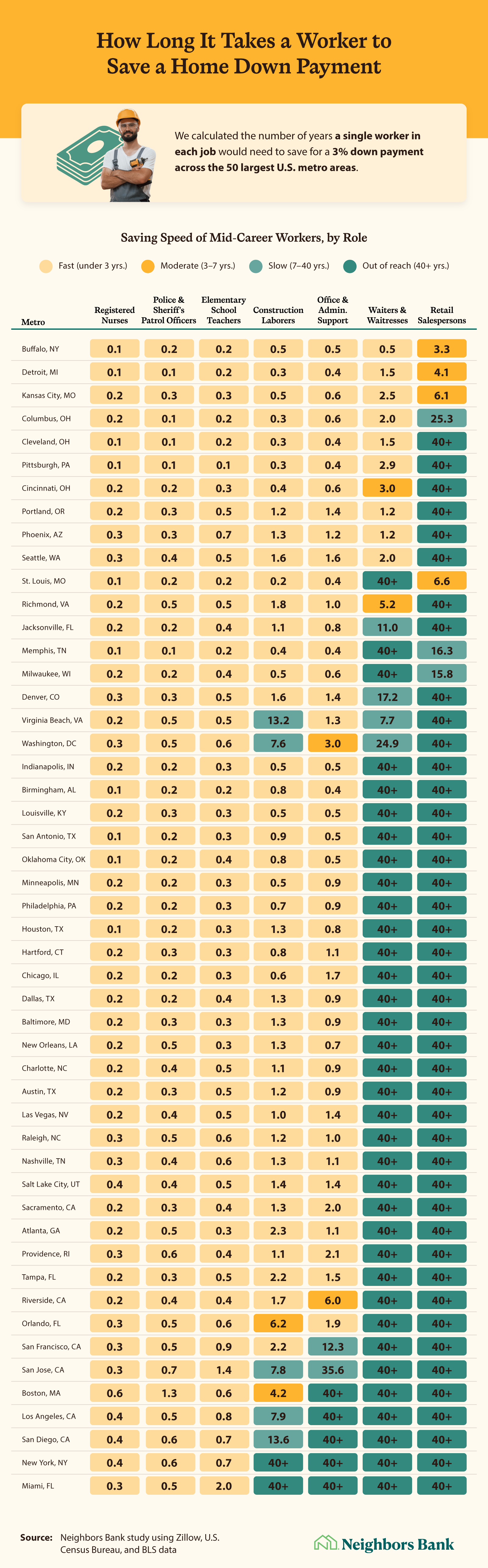

Registered nurses can save a 3% down payment on a starter home in under a year in all 50 of the largest U.S. metros.

Buffalo, NY; Detroit, MI; Kansas City, MO; and Columbus, OH are the most accessible metros for workers, with all seven occupations able to save for a 3% down payment in these locations.

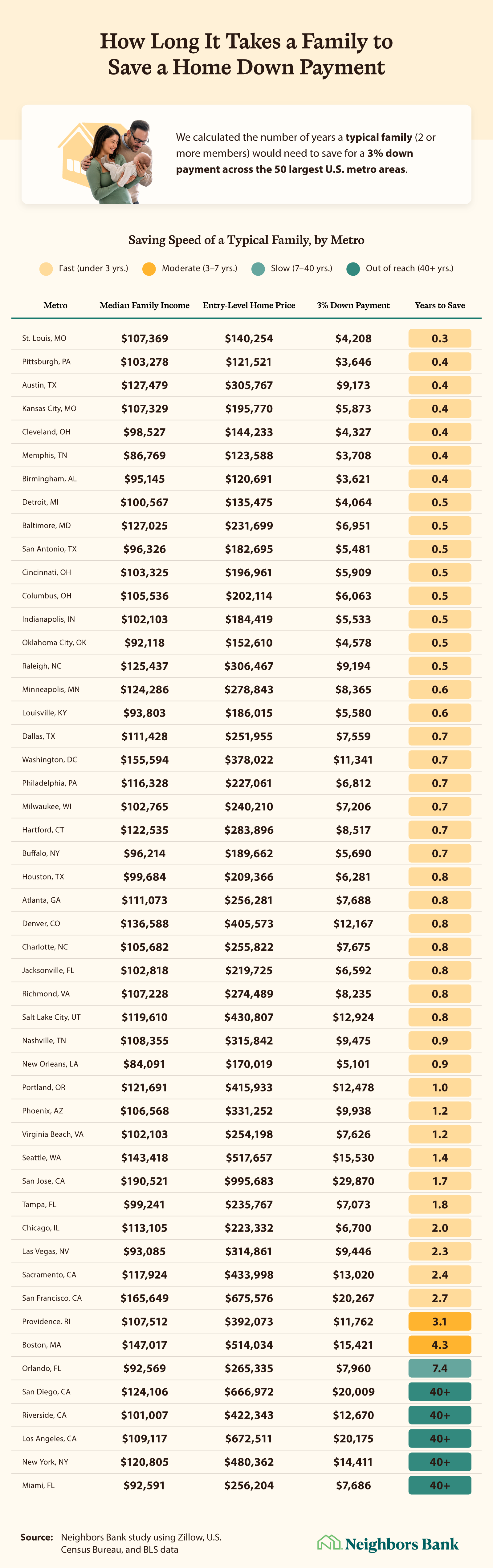

A typical family with two or more members can save for a 3% down payment within one year in 32 of the 50 largest metros.

Families can save a down payment in less than six months in seven of the 50 largest metros, the fastest being St. Louis, MO (less than four months).

A note on the trade-offs: a smaller down payment means more of the home is financed, so a 3% down loan typically comes with private mortgage insurance (PMI) and a higher monthly payment than putting more down. PMI can usually be canceled once you reach 20% equity. The right down payment depends on your budget and goals; a 3% option lowers the upfront hurdle, not the total cost of the home.

Individual results will vary based on income, expenses, savings, debt, and other personal financial factors. This analysis assumes 100% of income remaining after rent and basic living costs is saved toward a down payment, which may not be realistic for every household. It reflects metro-level medians and representative scenarios only, and is not a projection or guarantee for any individual borrower. See the Methodology section below for full data sources and calculation details.

Where Workers Have a Path to Homeownership

To see how homeownership stacks up for working Americans, we looked at these common, widely held jobs across the country:

Registered nurses

Police and sheriff's patrol officers

Elementary school teachers

Construction laborers

Office and administrative support workers

Waiters and waitresses

Retail salespersons

These roles span a range of wages and are found in every metro we studied, which makes them a useful way to compare how far a paycheck goes from one market to the next. To estimate how long saving takes, we started with each job's local median pay, subtracted typical rent and everyday living costs, and measured how long the leftover would take to add up to a 3% down payment on a local starter home.

Buffalo, Detroit, Kansas City, and Columbus stood out as the most attainable metros for workers. In each of these cities, all seven analyzed occupations could save for a starter home with a 3% down payment. Higher-wage workers also fared well across the board:

Registered nurses can save a 3% down payment on a starter home in under a year in all 50 of the largest U.S. metros.

Police and sheriff's patrol officers can do it within 1.3 years.

Elementary school teachers can reach 3% savings in 2 years or less.

If you're wondering whether homeownership is possible for you, you're not alone. In markets where saving feels out of reach, down payment assistance programs can help bridge the gap.

How Quickly Can a Typical Family Save for a Down Payment?

For families earning the median family income in their metro, the path to a down payment varies widely by locale. We applied the same approach here, using each metro's median family income in place of a single worker's wage. In many cities, homeownership is a realistic near-term goal.

Families can save for a down payment within one year in 32 of the 50 largest metros. St. Louis, Pittsburgh, Austin, Kansas City, and Cleveland were among the fastest metros for 3% down payment savings, allowing a typical family to save enough in less than six months. These markets combine relatively affordable home prices with median incomes that leave room for savings after covering everyday expenses.

What Home Affordability Looks Like Today

The path to homeownership looks different depending on your income and where you live. For many workers and families, a down payment is achievable within months. For others, it may take longer, but that doesn't mean homeownership is out of reach. Also, keep in mind that the down payment isn't the only upfront cost. You'll also need to factor in closing costs, typically 3% to 6% of the loan amount.

Down payment and closing cost assistance can reduce what you need upfront, and loan options for first-time homebuyers may put homeownership closer than you think. Neighbors Bank can help you find programs you qualify for based on your income, location, and goals.

Methodology

This study estimates how long it would take to save for a home down payment, both for a single worker in seven occupations and for a typical family (two or more related persons), across the 50 most populous U.S. metropolitan areas. Drawing exclusively from publicly available federal and industry datasets, it compares local wages and incomes against local home prices, rents, and living costs to show where buying a home is within reach and where it isn't.

Occupations analyzed: Seven occupations were selected to represent common, widely held jobs: elementary school teachers, registered nurses, police and sheriff's patrol officers, office and administrative support workers, construction laborers, waiters and waitresses, and retail salespersons.

Each occupation was defined by its federal Standard Occupational Classification code. Wages reflect each occupation's median annual wage (50th percentile) in each metro, which represents a typical mid-career worker rather than an entry-level or senior one. Actual pay varies with experience, employer, and location.

Data sources:

Wages: Bureau of Labor Statistics, Occupational Employment and Wage Statistics, May 2025; annual median wage by occupation and metro.

Family income: U.S. Census Bureau, American Community Survey 2024 (1-year), median family income by metro; families defined as two or more related persons.

Home values: Zillow Home Value Index, bottom-tier (starter homes), seasonally adjusted, April 2026.

Rent: Zillow Observed Rent Index, all homes plus multifamily, April 2026.

Living costs: Bureau of Labor Statistics, Consumer Expenditure Survey, 2024 (non-housing spending by income); adjusted to each metro using Bureau of Economic Analysis Regional Price Parities, 2024.

Down payment benchmark: 3% of the home price; the entry-level minimum available to first-time homebuyers under common conventional mortgage programs.

How the figures are calculated: For each worker (or family) in each metro, monthly take-home pay is the median annual wage (or median family income), minus estimated taxes, divided by 12. From take-home pay, two costs are subtracted: rent and a cost-of-living figure for everything else.

Rent for the single worker is set to a one-bedroom level, reflecting a single renter rather than a whole household. Because Zillow does not publish a separate one-bedroom rent series, each metro's typical rent is scaled to a one-bedroom using the national ratio of one-bedroom median rent to the typical all-homes rent (roughly 78%, based on April 2026 figures). For the family analysis, the full typical local rent is used.

Cost of living covers non-housing essentials (food, transportation, healthcare, and other basics). Rather than a flat figure, it scales with income (interpolated from the Consumer Expenditure Survey's 2024 spending levels by income) applied per person for the single worker and at the household level for the family, then adjusted to each metro by a non-housing price index (BEA Regional Price Parities for goods and non-housing services). The all-items price level is deliberately not used, to avoid double-counting local housing costs already captured in rent.

Whatever remains after rent and living costs is the monthly amount available to save. To calculate the time to save a down payment, that monthly amount is applied to the target down payment (3% of the metro's starter-home price), assuming 100% of what's left is banked.

Data notes:

The analysis models two cases: a single earner saving alone, and a typical family on its median income.

A case is recorded as "40+" when rent and basic living costs equal or exceed take-home pay (leaving nothing to save), or when saving the down payment would take more than 40 years.

Living costs scale with income but are not otherwise varied between occupations within a metro. For the lowest-wage occupations, rent plus basic living costs can still exceed take-home pay, meaning the worker cannot save regardless of how they economize.

The 100% savings rate is a best case: it assumes every dollar left after rent and living costs goes toward the down payment. Most households save less, so real-world timelines will usually be longer.

Wages for tipped occupations (such as waiters and waitresses) may be understated in federal data, since tip income is often underreported.

Figures are at the metro level, not the city level, and reflect median wages and incomes. Individual earnings, household composition, existing savings, and outside financial support are not captured.

"Family" follows the U.S. Census Bureau definition of two or more related people living together. The analysis uses each metro's median family income and does not vary by family size; larger households typically face higher living costs, which would lengthen their saving timeline.

The figures measure only the time needed to save the down payment, not total wealth or earnings. Because a 3% down payment is a relatively small target, the difference in saving time between higher- and lower-earning occupations narrows at the fast end, so occupations with meaningfully different wages can show similar saving times in many metros.

Wages reflect each metro's current median annual wage and are a point-in-time snapshot. The analysis does not project future raises or account for differences in wage growth between occupations.

About Neighbors Bank

Neighbors Bank is a home loan lender dedicated to helping everyday Americans on the path to homeownership. Specializing in mortgage products designed for first-time homebuyers, Neighbors Bank combines competitive rates with a clear process so you can focus on finding the right home and not get lost in the paperwork.

Fair Use Statement

Feel free to share these findings for noncommercial purposes. If you reference this study, please provide attribution to Neighbors Bank and include a link back to the original source.