If you’re hoping to buy in a rural or suburban area and don’t have a large down payment saved, a USDA loan might be worth a closer look.

USDA loans are designed to help make homeownership more affordable and accessible in eligible communities. Like any loan program, they come with both benefits and limitations. Let’s walk through both so you can decide what fits your goals.

What Is a USDA Loan?

The United States Department of Agriculture (USDA) created this loan program to support homebuyers in eligible rural and suburban areas.

There are two types of USDA loans:

USDA Direct loans, funded directly by the USDA and designed for very low-income borrowers.

USDA Guaranteed loans, offered by private lenders (like Neighbors Bank) and backed by the USDA.

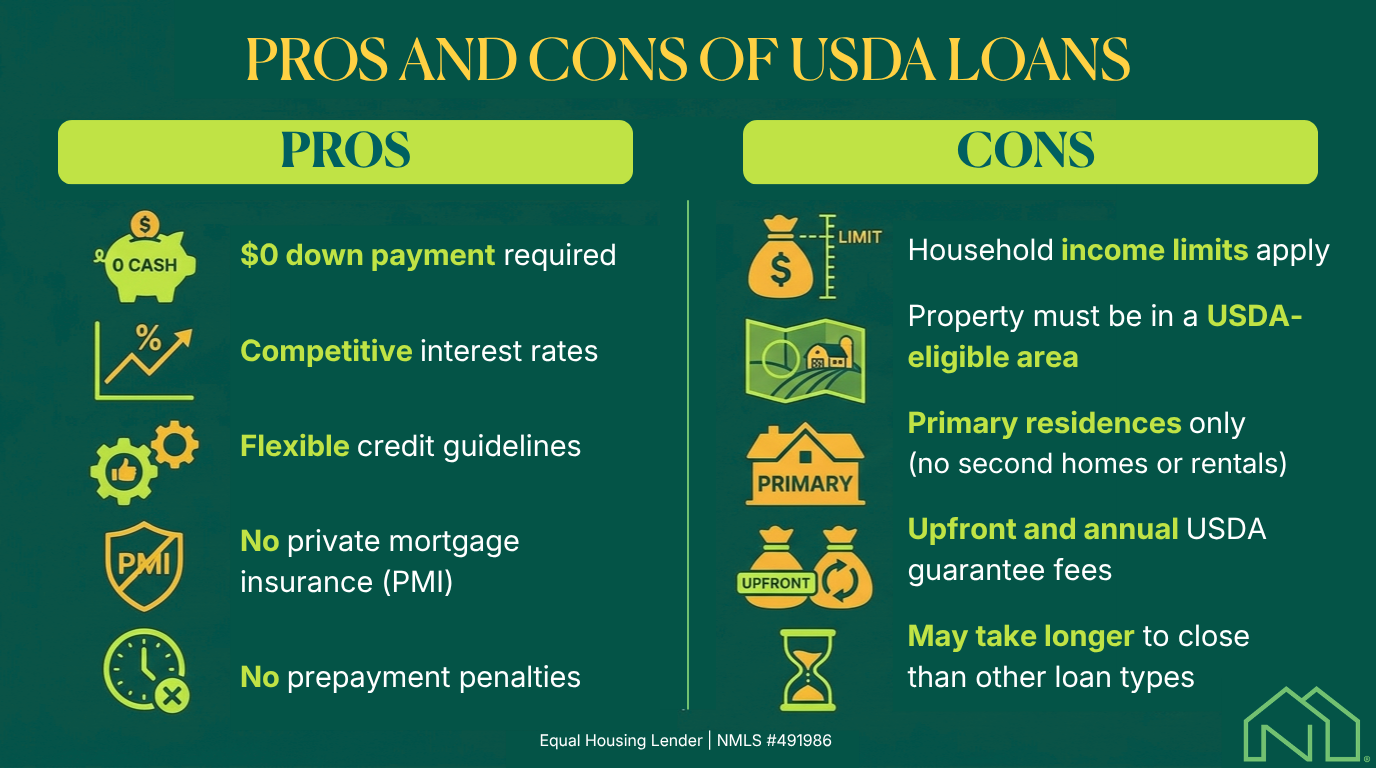

Most homebuyers use the USDA guaranteed loan program through a lender. Here’s a quick look at their pros and cons:

What Are the Benefits of a USDA Loan?

1. No Down Payment Required

One of the biggest advantages of a USDA loan is that you don’t need a down payment.

For many buyers, saving 10–20% feels like the biggest barrier to homeownership. USDA loans remove that hurdle, making it possible to buy sooner — even if you haven’t built up a large savings account yet.

You can still choose to put money down if you’d like, but it isn’t required.

2. Competitive Interest Rates

Because USDA loans are backed by the government, lenders can often offer competitive interest rates.

Over time, even a slightly lower rate can make a meaningful difference in your monthly payment and the total interest you pay.

3. Flexible Credit Guidelines

USDA loans don’t set one strict minimum credit score across the board. Many lenders look for a score around 640 for streamlined approval, but qualifying with a lower score may still be possible depending on your full financial picture.

At Neighbors Bank, we typically look for a minimum FICO score of 620 for USDA loans.

A credit score is just one part of the story. Your income, debt, and overall financial stability matter too.

4. No Private Mortgage Insurance (PMI)

Conventional loans usually require private mortgage insurance (PMI) if you put down less than 20%.

USDA loans don’t require PMI. Instead, they use a different fee structure (which we’ll explain below). For many buyers, this can mean a lower monthly payment compared to some conventional options.

5. No Prepayment Penalties

If you decide to pay extra toward your loan every month, or even pay it off early (USDA loans only offer 30-year terms), you won’t face a penalty.

That flexibility can help you save on interest over time if your financial situation changes.

What are the Disadvantages of a USDA Loan?

USDA loans can be a great option, but they aren’t for everyone. Here’s what to keep in mind.

1. Income Limits

To qualify, your total household income must generally fall within 115% of the median income for your area. See the local income limit for your area.

These limits are in place to ensure the program supports households it was designed to help. If your income is above the limit, you may need to explore other loan options.

2. Property Location Requirements

The home must be located in a USDA-eligible area. While the program is often described as “rural,” many suburban areas qualify, too. You might be surprised what’s eligible.

The home must also meet basic property standards to ensure it’s safe and livable.

3. Primary Residence Only

USDA loans are only intended for primary residences. You can’t use them to purchase a vacation home, second home, or investment property. You’ll also need to move into the home within 60 days of closing in most cases.

4. USDA Guarantee Fees

Instead of mortgage insurance, USDA loans include the guarantee fee. Here’s how it works:

An upfront guarantee fee (currently 1% of the loan amount)

An annual fee (currently 0.35% of the remaining loan balance), which is included in your monthly payment

Even with these fees, USDA loans are often more affordable than options that require private mortgage insurance.

5. Longer Processing Timeline

Because USDA loans require additional approval steps (including review for property eligibility and income limits), they can sometimes take a little longer to close compared to conventional loans.

Planning ahead and submitting documents promptly can help keep things moving so that you can close on time.

Are USDA loans a good idea?

A USDA loan may be a strong fit if:

You meet the income guidelines

You’re buying a primary residence

The property is in an eligible location

The right choice depends on your finances, your location, and your long-term goals. If you want to learn about your eligibility or other loan options, get started here and a loan expert can help you see what’s possible.

Are USDA Loans a Good Idea?

A USDA loan may be a strong fit if:

You meet the income guidelines

You’re buying a primary residence

The property is in an eligible location

The right choice depends on your finances, your location, and your long-term goals. If you want to learn about your eligibility or other loan options, get started here and a loan expert can help you see what’s possible.

Frequently Asked Questions

What makes USDA loans more affordable?

USDA loans can offer lower monthly payments thanks to competitive interest rates and no private mortgage insurance. Instead, they use a modest annual fee, often less expensive than PMI.

Do USDA loans really require no down payment?

Yes. One of the biggest advantages is the $0 down payment requirement for eligible buyers. However, like all mortgages, USDA loans have closing costs that you should plan for in advance.

What are the biggest limitations of USDA loans?

The main restrictions are income limits, property location rules, and primary residence requirements. USDA loans also sometimes take longer to process, which can be very difficult for buyers with short timelines.

Are USDA fees better than mortgage insurance?

The monthly USDA guarantee fee costs less than PMI on average, however, the guarantee fee lasts for the life of the loan, while PMI cancels automatically once you have 22% equity in the home.

Emily Kittle is an experienced underwriter with a strong background in risk assessment, training, and loan decision-making. She excels at solving complex mortgage challenges and guiding loans to closing using creativity and critical thinking.